Nvidia posts booming revenue and positive guidance

Jamie Dutta >

Market Analyst

Jamie Dutta >

Market Analyst

Jamie Dutta is a Market Analyst for Vantage. He comes with extensive experience as a full-time trader and financial market commentator, having worked as a trader in top tier investment banks and trading houses.

* US stocks close slightly higher with Nvidia on deck

* Dollar surges to two-week high, extended vs yen ahead of NFP

* Gold choppy and trims gains after FOMC minutes

* NVDA quiets investor fears with upbeat guidance, stock futures up

FX: USD broke higher and hit the 200-day SMA at 100.29. This capped the upside earlier in the month at 100.36. Rate cut expectations were pared back after the BLS schedule showed that the Fed won’t see the November or October US jobs data before the December FOMC meeting. Money markets predict a one in three chance now of a 25bps rate reduction, versus a 50:50 chance on Tuesday. The FOMC minutes added little new but emphasised how divided the committee is. The greenback was modestly bid on the release as ‘many’ officials were expecting no change in December.

EUR turned lower for a fourth day in a row but outperformed its peers. A minor Fib level (23.6%) of this year’s rally is 1.1507. Final euro area inflation figures printed in line with estimates, with the headline holding steady at 2.1% y/y and core at 2.4% y/y. The data didn’t change the outlook for euro area interest rates. Markets still price no material change in the ECB’s policy settings through to Autumn 2026.

GBP was mid pack among the majors again after inflation data revealed that food price pressures were strong and services CPI rose after volatile items are stripped out. But many economists believe UK inflation has peaked and markets still price in a high chance of a December BoE rate cut. The November multi-month lows sit at 1.3010.

JPY was a major underperformer again as USD/JPY rose to levels last seen in mid-January. Concerns mounted about the BoJ’s independence and its implications on the outlook for relative central bank policy following comments from Finance Minister Katayama who stated an intention to adjust the BoJ/government accord. These was also some speculation that the BoJ is unlikely to raise rates before March. JGB yields had hit multi-year highs overnight on fears the new stimulus fiscal package will strain already weak public finances.

US stocks: The S&P 500 added 0.38%, closing at 6,642. The Nasdaq moved higher by 0.56% to finish at 24,641. The Dow settled up 0.1% at 46,139. Tech, Communication Services, Materials and Financials led the gainers with Energy the notable laggard. News of a proposed peace plan by the US to end the Ukraine/Russia war hit the latter sector and crude. Communications were boosted by fresh all time highs in Alphabet on positive reviews of the new Gemini 3. This came on the back of Berkshire Hathaway and Warren Buffet’s switch into Google’s parent and out of Apple. Three big retailers (TGT, LOW and TJX) reported earnings with mixed results. Only TJX closed higher after giving strong full year guidance. Target trimmed the top end of its full-year profit range and closed 2.8% lower. Nvidia forecast Q4 revenues above estimates – $65bn vs $61.66bn and adjusted gross margins above expectations. The stock rose 4% in extended trading, with US futures also trading positively.

Asian stocks: Futures are mixed. Stocks were cautious ahead of big risk events ahead. The ASX 200 was supported by gold miner gains, but limited news flow saw prices settle virtually unchanged. The Nikkei 225 dipped again in choppy trade amid ongoing China-Japan tensions and PM Takaichi’s fiscal package. The Hang Seng and Shanghai Composite was muted after initial gains with Hong Kong conforming to global tech losses.

Gold sold off through the US session, having climbed over 1% higher earlier in the day. The dollar got increasingly bid as Treasury yields eventually turned higher on the BLS news. A major Fib retracement level (38.2%) of the early September break to the record high in November sits at $4,044.

Day Ahead – US Non-Farm Payrolls, Japan CPI

Consensus estimates of the delayed September US employment data are for the headline to add 50k jobs, with an unemployment rate steady at 4.3% and average hourly earnings at 0.3% m/m and 3.7% y/y. Alternative labour market data have painted a mixed picture with jobs growth sluggish but not falling off a cliff. An inline print might be seen as a ‘Goldilocks’ report – not too hot to ignite inflation fears and not too cold that growth fears increase.

October nationwide Japan inflation is expected to accelerate driven by broad-based goods and services price gains. Tokyo CPI has been hot in recent months, and this could cause the 30% chance of a December BoJ interest rate hike to increase.

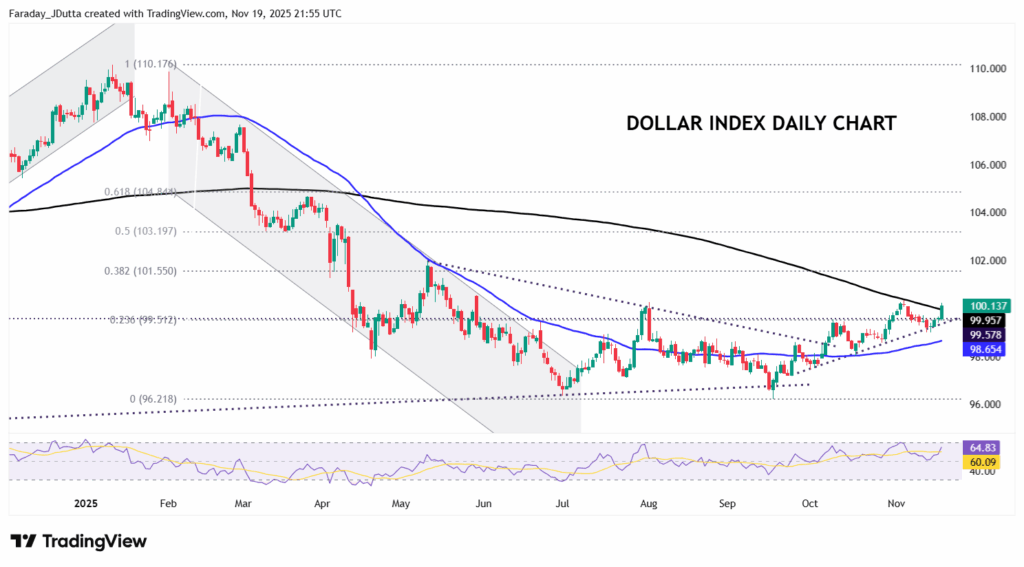

Chart of the Day – Dollar upside move through the 200-day SMA

The greenback has enjoyed four consecutive days of buying after the Dollar Index found support at the upward trendline from the late September low last week. A very strong NFP report may push the Fed to the sidelines and see more dollar strength. The 200-day SMA sits at 99.95 with next resistance at the November and August tops at 100.36/25. Very soft NFP could spark recession or stagflation fears and cause the buck to get sold as Fed rate cut bets increase. Support sits at that upward trendline and the long-term July low from 2023 around 99.57.